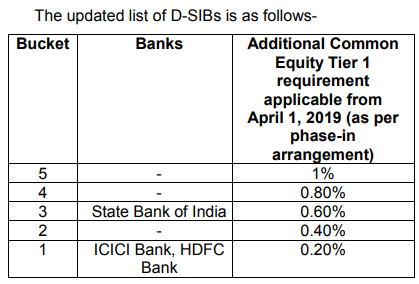

What is a D-SIB? 1. Some banks, due to their size, cross-jurisdictional activities, complexity, lack of substitutability and interconnectedness, become systemically important. The disorderly failure of these banks has the potential to cause significant disruption to the essential services they provide to the banking system, and in turn, to the overall economic activity. Therefore, the continued functioning of Systemically Important Banks (SIBs) is critical for the uninterrupted availability of essential banking services to the real economy. Lessons from recent global financial crisis: 2. It was observed during the recent global financial crisis that problems faced by certain large and highly interconnected financial institutions hampered the orderly functioning of the financial system, which in turn, negatively impacted the real economy. Government intervention was considered necessary to ensure financial stability in many jurisdictions. Cost of public sector intervention and consequential increase in moral hazard required that future regulatory policies should aim at reducing the probability of failure of SIBs and the impact of the failure of these banks. 3. As a response to the recent crisis, a series of reform measures were unveiled, broadly known as Basel III, to improve the resiliency of banks and banking systems. Basel III reform measures include: increase in the quality and quantity of regulatory capital of the banks, improving risk coverage, introduction of a leverage ratio to serve as a backstop to the risk-based capital regime, capital conservation buffer and countercyclical capital buffer as well as a global standard for liquidity risk management. These policy measures will cover all banks including SIBs. However, these policy measures are not adequate to deal with risks posed by SIBs. Therefore, additional policy measures for SIBs are necessary to counter the systemic risks and moral hazard issues posed by these banks, which other policy reforms do not address adequately. Additional risks posed by SIBs: 4. SIBs are perceived as banks that are ‘Too Big To Fail (TBTF)’. This perception of TBTF creates an expectation of government support for these banks at the time of distress. Due to this perception, these banks enjoy certain advantages in the funding markets. However, the perceived expectation of government support amplifies risk-taking, reduces market discipline, creates competitive distortions, and increases the probability of distress in the future. These considerations require that SIBs should be subjected to additional policy measures to deal with the systemic risks and moral hazard issues posed by them. 5. In October 20101, the Financial Stability Board (FSB) recommended that all member countries needed to have in place a framework to reduce risks attributable to Systemically Important Financial Institutions (SIFIs) in their jurisdictions. The FSB asked the Basel Committee on Banking Supervision (BCBS) to develop an assessment methodology comprising both quantitative and qualitative indicators to assess the systemic importance of Global SIFIs (G-SIFIs), along with an assessment of the extent of going-concern loss absorbency capital which could be provided by various proposed instruments. In response, BCBS came out with a framework in November, 2011 (since up-dated in July, 2013) for identifying the Global Systemically Important Banks (G-SIBs) and the magnitude of additional loss absorbency capital requirements applicable to these G-SIBs. 6. The BCBS is also considering proposals such as large exposure restrictions and liquidity measures which are referred to as “other prudential measures” in the FSB Recommendations and Time Lines. The G20 leaders had asked the BCBS and FSB in November 2011 to extend the G-SIBs framework to Domestic Systemically Important Banks (D-SIBs) expeditiously. 7. The methodology to be used to assess the systemic importance is largely based on the indicator based approach being used by BCBS to identify G-SIBs. The indicators to be used to assess domestic systemic importance of the banks are as follows: i) Size; ii) Interconnectedness; iii) Lack of readily available substitutes or financial institution infrastructure; and iv) Complexity. What is CET1 (Common Equity Tier 1)? % CET1 is a measure of bank solvency that gauges a bank’s capital strength. % This measure is better captured by the CET1 ratio, which measures a bank’s capital against its assets. % Common equity Tier 1 ratio = common equity tier 1 capital / risk-weighted assets According to Press Release of March 14, 2019 RBI releases 2018 list of Domestic Systemically Important Banks (D-SIBs). SBI, ICICI Bank, and HDFC Bank continue to be identified as Domestic Systemically Important Banks (D-SIBs), under the same bucketing structure as last year. The additional Common Equity Tier 1 (CET1) requirement for D-SIBs has already been phased-in from April 1, 2016 and will become fully effective from April 1, 2019. The additional CET1 requirement will be in addition to the capital conservation buffer.Background: The Reserve Bank had issued the Framework for dealing with Domestic Systemically Important Banks (D-SIBs) on July 22, 2014. The D-SIB framework requires the Reserve Bank to disclose the names of banks designated as D-SIBs starting from 2015 and place these banks in appropriate buckets depending upon their Systemic Importance Scores (SISs). Based on the bucket in which a D-SIB is placed, an additional common equity requirement has to be applied to it. In case a foreign bank having branch presence in India is a Global Systemically Important Bank (G-SIB), it has to maintain additional CET1 capital surcharge in India as applicable to it as a G-SIB, proportionate to its Risk Weighted Assets (RWAs) in India i.e. additional CET1 buffer prescribed by the home regulator (amount) multiplied by India RWA as per consolidated global Group books divided by Total consolidated global Group RWA. The higher capital requirements are applicable from April 1, 2016 in a phased manner and will become fully effective from April 1, 2019. The additional common equity requirement for different buckets over the four year phase-in period is as under: Based on the methodology provided in the D-SIB framework and data collected from banks as on March 31, 2015 and March 31, 2016, the Reserve Bank had announced State Bank of India and ICICI Bank Ltd. as D-SIBs on August 31, 2015 and August 25, 2016, respectively. Based on data collected from banks as on March 31, 2017, the Reserve Bank had announced State Bank of India, ICICI Bank Ltd. and HDFC Bank Ltd. as D-SIBs on September 04, 2017. Current update is based on the data collected from banks as on March 31, 2018. Further the D-SIB framework requires that “The assessment methodology for assessing the systemic importance of banks and identifying D-SIBs will be reviewed on a regular basis. However, this review will be at least once in three years.” Current review and analysis of cross country practices do not warrant any change in the extant framework at present. References % Framework for Dealing with Domestic Systemically Important Banks (D-SIBs) % 2017 list of global systemically important banks (G-SIBs) (From: fsb.org) % RBI releases Framework for dealing with Domestic Systemically Important Banks (D-SIBs) / Date : Jul 22, 2014 % RBI releases list of Domestic Systemically Important Banks (D-SIBs) / Date : Aug 31, 2015 % RBI identifies SBI and ICICI Bank as D-SIBs in 2016 / Date : Aug 25, 2016 % RBI releases 2017 list of Domestic Systemically Important Banks (D-SIBs) / Date : Sep 04, 2017 % RBI releases 2018 list of Domestic Systemically Important Banks (D-SIBs) / Date : Mar 14, 2019 % Common Equity Tier 1 (CET1)

Based on the methodology provided in the D-SIB framework and data collected from banks as on March 31, 2015 and March 31, 2016, the Reserve Bank had announced State Bank of India and ICICI Bank Ltd. as D-SIBs on August 31, 2015 and August 25, 2016, respectively. Based on data collected from banks as on March 31, 2017, the Reserve Bank had announced State Bank of India, ICICI Bank Ltd. and HDFC Bank Ltd. as D-SIBs on September 04, 2017. Current update is based on the data collected from banks as on March 31, 2018. Further the D-SIB framework requires that “The assessment methodology for assessing the systemic importance of banks and identifying D-SIBs will be reviewed on a regular basis. However, this review will be at least once in three years.” Current review and analysis of cross country practices do not warrant any change in the extant framework at present. References % Framework for Dealing with Domestic Systemically Important Banks (D-SIBs) % 2017 list of global systemically important banks (G-SIBs) (From: fsb.org) % RBI releases Framework for dealing with Domestic Systemically Important Banks (D-SIBs) / Date : Jul 22, 2014 % RBI releases list of Domestic Systemically Important Banks (D-SIBs) / Date : Aug 31, 2015 % RBI identifies SBI and ICICI Bank as D-SIBs in 2016 / Date : Aug 25, 2016 % RBI releases 2017 list of Domestic Systemically Important Banks (D-SIBs) / Date : Sep 04, 2017 % RBI releases 2018 list of Domestic Systemically Important Banks (D-SIBs) / Date : Mar 14, 2019 % Common Equity Tier 1 (CET1)

Thursday, December 31, 2020

Domestic Systematically Important Banks of India as of Jan, 2021

Subscribe to:

Post Comments (Atom)

Social media users scroll rapidly, so if content doesn’t hook them instantly, it’s lost. Digital Marketing in Faridabad guided us on using bold hooks, clean designs, and focused storytelling that grips attention immediately. Designyze also helped shorten caption introductions and highlight benefits upfront. This small creative refinement significantly improved our retention rate.

ReplyDelete